VA Home Loans: Streamlining the Home Acquiring Refine for Military Personnel

VA Home Loans: Streamlining the Home Acquiring Refine for Military Personnel

Blog Article

The Necessary Guide to Home Loans: Opening the Benefits of Flexible Financing Options for Your Dream Home

Browsing the intricacies of home car loans can usually really feel challenging, yet comprehending versatile financing options is important for potential property owners. VA Home Loans. With a variety of funding types offered, including adjustable-rate mortgages and government-backed options, consumers can customize their funding to line up with their private financial situations.

Recognizing Home Loans

Comprehending home finances is necessary for potential property owners, as they represent a substantial monetary commitment that can influence one's monetary health for years to come. A home mortgage, or home loan, is a sort of debt that permits individuals to obtain money to acquire a property, with the building itself offering as security. The loan provider provides the funds, and the consumer accepts repay the lending quantity, plus rate of interest, over a specific duration.

Key parts of mortgage include the major amount, interest rate, financing term, and month-to-month settlements. The principal is the original lending quantity, while the rate of interest establishes the cost of loaning. Lending terms typically range from 15 to three decades, affecting both monthly settlements and general interest paid.

Kinds of Flexible Financing

Adaptable financing options play a critical role in fitting the diverse requirements of homebuyers, enabling them to tailor their mortgage services to fit their economic circumstances. Among the most widespread kinds of adaptable funding is the variable-rate mortgage (ARM), which supplies a preliminary fixed-rate period followed by variable rates that change based upon market conditions. This can supply lower initial payments, interesting those that expect earnings development or strategy to relocate prior to prices change.

An additional option is the interest-only mortgage, permitting debtors to pay just the interest for a specific period. This can cause lower month-to-month settlements originally, making homeownership more accessible, although it may lead to bigger settlements later on.

In addition, there are additionally hybrid loans, which integrate functions of dealt with and adjustable-rate mortgages, providing security for a set term adhered to by adjustments.

Last but not least, government-backed loans, such as FHA and VA fundings, use flexible terms and lower deposit demands, satisfying first-time customers and professionals. Each of these options offers special benefits, allowing homebuyers to pick a financing remedy that aligns with their lasting economic objectives and individual situations.

Benefits of Adjustable-Rate Mortgages

Just how can variable-rate mortgages (ARMs) profit homebuyers looking for cost effective funding options? ARMs use the potential for lower initial rates of interest compared to fixed-rate description home mortgages, making them an eye-catching choice for customers wanting to decrease their month-to-month payments in the early years of homeownership. This preliminary duration of lower prices can dramatically enhance price, permitting property buyers to spend the financial savings in various other concerns, such as home renovations or cost savings.

In addition, ARMs often include a cap structure that restricts just how a lot the rate of interest can increase during change durations, offering a degree of predictability and defense versus severe changes in Click Here the marketplace. This attribute can be particularly helpful in a climbing rate of interest atmosphere.

In Addition, ARMs are optimal for purchasers that plan to refinance or market before the finance readjusts, enabling them to maximize the reduced prices without direct exposure to possible price boosts. As a result, ARMs can function as a tactical economic tool for those who are comfy with a level of threat and are looking to maximize their buying power in the existing real estate market. Generally, ARMs can be a compelling alternative for savvy property buyers looking for versatile financing options.

Government-Backed Finance Choices

FHA lendings, guaranteed by the Federal Housing Administration, are ideal for first-time property buyers and those with reduced credit report. They commonly require a lower deposit, making them a popular choice for those who may battle to conserve a significant amount for a traditional financing.

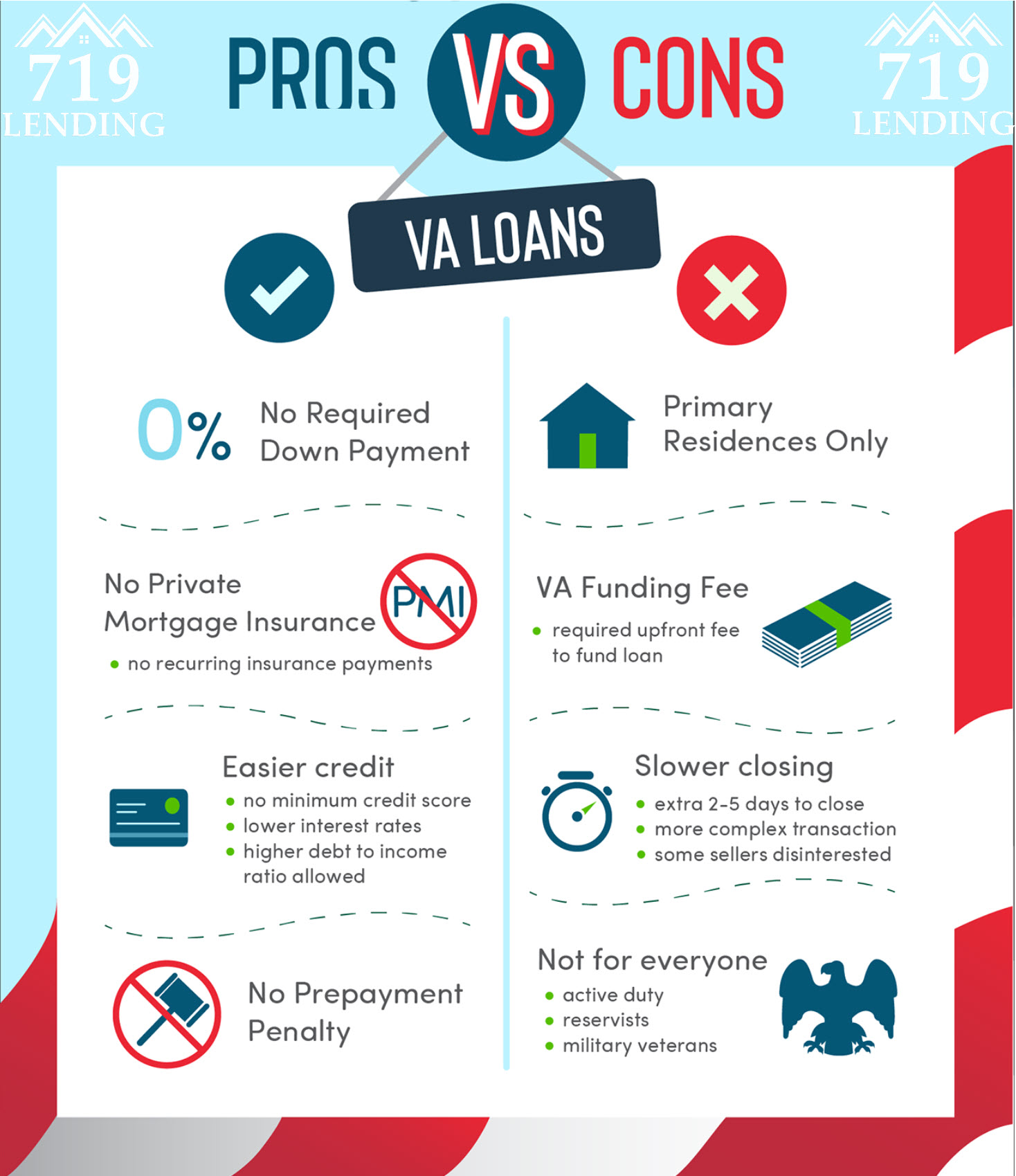

VA finances, available to veterans and active-duty military employees, offer positive terms, including no exclusive mortgage and no down repayment insurance (PMI) This makes them an eye-catching alternative for eligible debtors looking to buy a home without the worry of extra costs.

Tips for Choosing the Right Financing

When evaluating car loan choices, debtors commonly take advantage of extensively assessing their economic scenario and lasting goals. Begin by identifying your budget plan, which consists of not only the home acquisition price however also added prices such as property click here for more info taxes, insurance policy, and upkeep (VA Home Loans). This extensive understanding will lead you in picking a finance that fits your financial landscape

Next, think about the kinds of car loans readily available. Fixed-rate mortgages offer stability in regular monthly repayments, while adjustable-rate home mortgages may offer lower preliminary prices yet can rise and fall in time. Analyze your risk resistance and exactly how long you intend to remain in the home, as these variables will certainly affect your lending selection.

Additionally, scrutinize rates of interest and fees connected with each loan. A lower rate of interest can significantly reduce the total cost over time, but be conscious of shutting prices and various other charges that could counter these financial savings.

Conclusion

In verdict, browsing the landscape of home mortgage exposes various flexible financing alternatives that satisfy diverse borrower demands. Recognizing the ins and outs of different finance types, including government-backed car loans and adjustable-rate home loans, enables educated decision-making. The benefits offered by these funding techniques, such as lower initial payments and customized benefits, inevitably improve homeownership ease of access. An extensive assessment of readily available choices guarantees that possible house owners can secure one of the most suitable funding solution for their special financial scenarios.

Navigating the complexities of home fundings can often feel challenging, yet recognizing adaptable financing choices is crucial for potential house owners. A home finance, or home loan, is a kind of financial debt that allows individuals to borrow money to acquire a residential property, with the property itself offering as collateral.Key elements of home financings consist of the primary quantity, rate of interest rate, funding term, and month-to-month settlements.In verdict, browsing the landscape of home financings discloses various flexible funding alternatives that provide to varied debtor requirements. Comprehending the ins and outs of different finance types, including government-backed fundings and adjustable-rate mortgages, enables informed decision-making.

Report this page